Project - 2023 - Market Analysis Procedures (D) Working Group

- 4. Possible NAIC Recommendations for Amending the Uniform Securities Act

- a. At the present time, the NAIC, including the Securities and Insurance Regulation Task Force, is studying the many "new-life" insurance products that are being sold by approximately 30 insurance companies.

- Simultaneously, the NAIC is considering whether changes in existing insurance laws are warranted as they apply to such products.

- It is also surveying its various member states to determine whether they have encountered problems with respect to these products.

- However, to date, no specific abuses or consumer problems have been brought to the attention of the Securities and Insurance Regulation Task Force.

1982-2, NAIC Proceedings

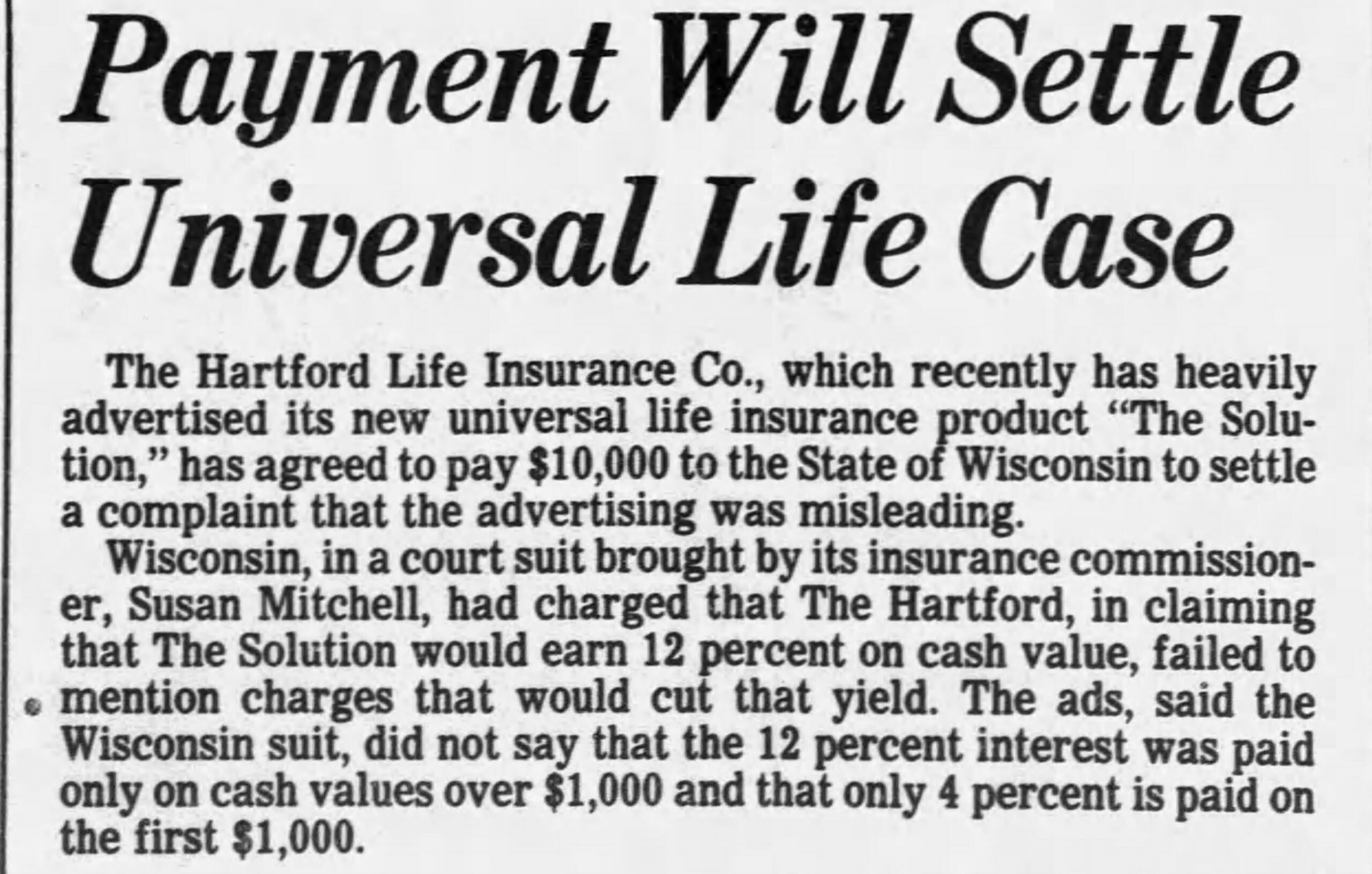

1982-Hartford-Life-UL-Mitchell-Wis-Hartford_Courant_Tue__Jun_8

- William Koenig (Northwestern Mutual) suggested that the parties all needed a common understanding of the terms used in their discussion. (p655)

1993-4, NAIC Proceedings - Life Disclosure Working Group – NAIC

- 2023 - AAA - Life Perspectives, Winter/Spring 2023 - [link]

- Donna Claire - Chair - Life Experience Committee

- Linda Lankowski - Chair - PBR Implementation Work Group

- Dave Sandberg - gave a life perspective in a general session that focused on big data, analytics, and artificial intelligence (AI) issues.

- Actuarial

- AAA

- Society of Actuaries Archives

- Policy Mechanics

- Media

- Magazines

- Newspapers

- VIDEO

- Law

- Legal Cases

- Words and Concepts

- NAIC

- Proceedings

- Government

- CBO - Congressional Budget Office

- CRS - Congressional Research Service

- Hearings - House and Senate

- FSOC - Financial Stability Oversight Council

- GAO - Government Accountability Office

- Issues

- Education

- Expectations / Mis-Selling

- LIRP

- Premiums, Values and Benefits

-

- Private Equity

- Runs

- Solvency

- Guaranty Associations - NOLHGA - National Organization of Life and Health Insurance Guaranty Associations

- Systemic Risk

- 2020 - AP - Exploring Universal Life Insurance - Actuarial - 47p

- Abstract

- This project focused on exploring Universal Life insurance by learning about its history, components, and process of reserving.

- To conduct our research, we read several textbooks, study notes and a Valuation Manual.

- We then created an Excel deliverable of a theoretical UL policy, created a Lesson plan about UL to teach to actuarial students, and a paper that explains the ins and outs of UL from a consumer standpoint and how the mechanics of a UL policy would work for a potential policyholder.

- Abstract

- Market Analysis Procedures (D) Working Group

- ... in gaining a life insurance education, one problem does present itself... the basic question is where to begin. (p1)

- 1961 - Book - Modern Life Insurance, by Robert I. Mehr

- ...market conduct regulation deals with the treatment of people.

- 1995-4, NAIC Proceedings - 1995 1205 - Attachment Four-A - NAIC Market Conduct Regulation Guidelines, Final Draft: Dec. 5, 1995

- Problems spotted during a market conduct review can be a precursor to financial solvency concerns.

- 2005-3, NAIC Proceedings - (2005 0922) - Life Insurance and Annuities (A) Committee

- (p115) - Commissioner Voss said an issue has come up to the Market Analysis (D) Working Group about some products being offered that are a term life insurance policy with an annuity side fund.

- The issue first arose in sales on military bases, but it appears the products are being sold elsewhere.

- She requested that the A Committee review these products.

- (p115) - Commissioner Voss said an issue has come up to the Market Analysis (D) Working Group about some products being offered that are a term life insurance policy with an annuity side fund.

- 2021 0721 - NAIC - Presentation - Birny Birnbaum, Center for Economic Justice (CEJ) - Reimagining Market Analysis and Market Regulation Through Enhanced Data Collection and Analytics. Presentation to NAIC Market Regulation and Consumer Affairs (D) Committee - 92p

- AI Opportunities for Insurance Regulatory Market Analysis

- (p13) - Identify legal consumer outcomes that reflect consumer confusion or legal but unfair or deceptive practices?

- (p16) - Quite a bit of data and information, but two major problems for using these to develop AI for market analysis:

- Difficult to combine data for AI due to different time frames, different types / sources of data and lack of common analytic unit.

- No data for actual, granular consumer outcomes. MCAS woefully

inadequate for market analysis, generally, and for implementing an AI toolfor market analysis, specifically. Moreover, MCAS requires prior

identification of potential problems which the summary data are intended to identify – so confirmation bias has an outsized impact on the selection of data elements and breakouts to be included.

- 2011 - NAIC E-Reg Conference 2011

- 2008 0531 - Comments of the Center for Economic Justice, Proposal for Market Conduct Annual Statement Centralized Data Collection. Before the NAIC Consumer Liaison Committee

- 2004 1201 - NAIC - CEJ - Proposal for Centralized Data Collection and Baseline Analysis of Market Performance Data, Submitted by the Center for Economic Justice

- AI Opportunities for Insurance Regulatory Market Analysis

- Project Goal

- .... preliminary step towards meeting the MAPWG goal 2)

- “In accordance with the second recommendation of the adopted Review of Artificial Intelligence Techniques in Market Analysis, assess currently available market analysis data to identify needed improvements in the effectiveness of the data for market analysis and the predictive abilities of the market scoring systems utilizing the data.”

- "Market Scoring Systems"

- Market Information Systems (D) Task Force - https://content.naic.org/cmte_d_market_information_systems.htm

- "Market Scoring Systems"

- “In accordance with the second recommendation of the adopted Review of Artificial Intelligence Techniques in Market Analysis, assess currently available market analysis data to identify needed improvements in the effectiveness of the data for market analysis and the predictive abilities of the market scoring systems utilizing the data.”

- .... preliminary step towards meeting the MAPWG goal 2)

- Project Documents

- 2021 1014 - NAIC - Review of Artificial Intelligence Techniques in Market Analysis - The Market Information Systems Research and Development (D) Working Group - 15p

- In addition, some of the techniques perform complex data mining operations, which can produce results that lack a clear interpretation

- 2023 0410 - NAIC Proceedings - MAPWG - Virtual Meeting - 9p

- (p5-7) - Potential Data Sources Used in Market Analysis

- 2021 1014 - NAIC - Review of Artificial Intelligence Techniques in Market Analysis - The Market Information Systems Research and Development (D) Working Group - 15p

- Law

- Government Hearings

- NAIC Proceedings

- Actuarial

- 2010-1, NAIC Proceedings - Principles-Based Reserving (EX) Working Group

- Paul Graham - ACLI - stated that the NAIC should condition a survey to determine the impact on the industry.

- He said he would be willing to assist the NAIC in developing and distributing such a survey, and suggested the NAIC hire an independent consultant to accumulate the results.

- Paul Graham - ACLI - stated that the NAIC should condition a survey to determine the impact on the industry.

- Commissioner Tyler said that because one consumer complaint often means that other consumers are also harmed by a particular practice, he would like to know the relationship between consumer complaints and proper market regulation.

- He said market regulators should leverage consumer-complaint data to ensure that what happens to one consumer is not happening to others.

- Mr. Mealer said complaints are included in the adopted market analysis process.

- Ms. Baker said the Market Regulation Handbook includes the use of consumer-complaint data in the market analysis process.

- Commissioner Ario said there are two methods of analyzing consumer complaints.

- He said the first method is to perform statistical analysis of the complaint data and the second method is to have ongoing discussions with a state’s complaint analysts.

- He said the consumer complaint analysts in a state are a “focus group” that each state should rely on.

- Mr. Narcini said that because the adopted processes included the use of consumer complaints, they are not specifically mentioned in the proposal.

- Commissioner Tyler said the requirement in the proposal that a state hold certain items confidential should be eliminated.

2009-3, NAIC Proceedings

- We designed commission rules that anticipated a relatively large number of rollovers of existing policies;.

- ...full commissions are paid provided the new Universal Life face amount is at least two times the face amount of the replaced policy..

-- Phillip B. Norton, not a member of the Society, is Vice President of The Lincoln National Life Insurance Company

1983 - SOA - Individual Life Insurance Retention and Replacement Strategies, Society of Actuaries - 24p

- 2003 - SOA - Current Events–Statutory, Society of Actuaries - 26p

- Mike Pickens, Arkansas Insurance Commissioner / NAIC - We want to publish a market analysis guide with instructions for using complaint data, financial data and market share information to target the most significant market problems.

- 2005 1117 - GOV (Senate) - A Review of the GAO Report on the Sale of Financial Products to Military Personnel --- [BonkNote] --- [PDF-89p]

- 2006 0711 - GOV (Senate) - Insurance Regulation Reform

- [PDF-152p, VIDEO-Senate-error] - <mp3, mp4> - R-yes

- NAIC - Alessandro Iuppa - Maine Superintendent of Insurance, President, National Association of Insurance Commissioners - Testimony - 40p

- CFA - Travis Plunkett, Legislative Director - Testimony - 47p

- 2007 1030 - GOV (House) - Additional Perspectives on the Need for Insurance Regulatory Reform, Paul Kanjorski (D-PA) --- [BonkNote]

- 2011 1207 - NAIC/FIO Meeting on Market Conduct, (Documents shared with FIO to facilitate discussion are attached) - 83p

-

- 1871-1, NAIC Proc.

- Gustavus W. Smith, Kentucky Insurance Commissioner: While on this subject, I may allude to what I consider the great trouble in life insurance.

- It is, in my opinion, an undoubted fact that educated, intelligent, influential business men of this country, as a class, are utterly ignorant of what this thing is.

- There is no such mystery in this that ordinary business men cannot learn it.

- If we can accomplish that with the people of this country—I do not mean all of them, only its leading, influential men to whom the people generally refer for advice, in reference to finance, law and other questions—I believe the institution is safe.

- You can then conduct your state supervision with some sort of safety.

- On the other hand, until these men do know all there is peculiar under this thing, all the state institutions that can be devised will not be able to hold this giant.

- The men interested in the life insurance business must know something what they are about; then they will be able to attend to their own business. (p128)

- If we can accomplish that with the people of this country—I do not mean all of them, only its leading, influential men to whom the people generally refer for advice, in reference to finance, law and other questions—I believe the institution is safe.

- Edwin W. Bryant, Actuary of the New York Insurance Department

- Why, there is not the least mystery in it.

- The only mystery is, how it has managed to live so long on the reputation of having a mystery, which it has not. [Laughter] (p128)

- Gustavus W. Smith, Kentucky Insurance Commissioner: While on this subject, I may allude to what I consider the great trouble in life insurance.

- 1914 - Academic - Conference on Life Insurance and Its Educational Relations, Published by the University of Illinois, Urbana - [PDF- p-GooglePlay]

-

No difference how well-intentioned and honest an insurance man's advice may be it may prove very expensive and harmful if not based on accurate knowledge. (p28)

-

-- Isaac Miller Hamilton, President of the Federal Life Insurance Company

-

-

- 1971-2, NAIC Proceedings - 1971 0616 - First Report of the Industry Advisory Committee to the NAIC B·S Subcommittee to Review the Model Unfair Trade Practices Act

- 3. The regulator already has the practical power to accomplish on behalf of the consumer what consumer class actions are designed to accomplish.

- This is evident from the testimony of Commissioner Barger in connection with Senate Bill 3201 in August 1970 (1970 NAIC Proceedings pages 135-144) and from Commissioner Durkin's testimony on S. 984, S. 1222 and S. 1378 in April, 1971;

- 4. Insurers will never be able to rely on the decision of the regulator. If policyholders are able to challenge the decision of the Commissioner through the use of the class action, the whole regulatory mechanism will be subverted.

- 5. Consumer class actions will result in "judicial" regulation of the insurance business;

- 3. The regulator already has the practical power to accomplish on behalf of the consumer what consumer class actions are designed to accomplish.

- 1972 - SOA - Life Insurance and the Buyer Anna Rappaport, Society of Actuaries - 2p-Article

- Until the buyer understands how the product works, attempts to compare price are essentially meaningless.

- 1973 / 1974 - GOV (Senate) - The Life Insurance Industry, Senator Philip Hart (D-MI) - Part 2 of 4 - [PDF-733p-GooglePlay]

- (p1501) - John Durkin (New Hampshire Insurance Commissioner): As a starting point, there is little regulation of the life insurance industry by the States.

- The States do little with respect to life insurance regulations for many reasons, mainly because there are very few problems with complaints over claims.

- Most of the staffs are involved with complaints relating to automobile insurance and health insurance.

- Life insurance is sort of the stepchild of many, if not most, insurance departments.

- (p1501) - John Durkin (New Hampshire Insurance Commissioner): As a starting point, there is little regulation of the life insurance industry by the States.

- 1979 - SOA - Future Trends and Current Developments in Individual Life Products (rsa79v5n44), Society of Actuaries - 24p

- Because of the high level of flexibility provided in a "Universal Life" style Adjustable Life product..... -- David R. Carpenter

- 1980 0207 - GOV - Federal Register - re: Class Action Lawsuits, FTC, McCarran-Ferguson Act - p2382

- Class Actions, Fraud, NAIC, States, Unfair

- Statement of John Durkin, Commissioner, State of New Hampshire, Insurance Department, Concord, N.H.; Accompanied By Jon S. Hanson, Executive Secretary, National Association of Insurance Commissioners (NAIC) - Senator John Durkin - (D-NH), (Former New Hampshire Insurance Commissioner)

- I ask unanimous consent, Mr. President, that my testimony in April 1971 before the Consumer Subcommittee of the Commerce Committee be printed in the RECORD at this point.

- While the NAIC has taken no position for or against class action, intense regulation on behalf of the consumer lessens the need for class action.

- Furthermore, the state provides an effective local, readily accessible complaint mechanism available to the consumer which serves as an alternative to class action.

- 1982 - Journal of Insurance Medicine - 1p

- Samuel H. Turner, President - The Life Insurance Company of Virginia

- Its fundamental "mechanics" are indistinguishable from those underlying traditional life insurance products.

- [Bonk: Its = Universal Life]

- Its fundamental "mechanics" are indistinguishable from those underlying traditional life insurance products.

- Samuel H. Turner, President - The Life Insurance Company of Virginia

- 1982-1, NAIC Proceedings - ACLI - Paper on Cost Disclosure for Universal Life - p399 - 4p

- An additional item of information that is recommended to be required in the policy summary is the point at which the policy will expire based on the policy guarantees and the anticipated premiums shown in the summary.

- 1982 - SOA - Universal Life (rsa82v8n111), Society of Actuaries - 14p

- Maybe he is not getting all the disclosure he needs, as far as the continuing benefit is concerned, when the interest rates change from that illustrated.

- Gary P. Monnin, Senior Vice President, Chief Actuary of American Founders Life Insurance Company

- Maybe he is not getting all the disclosure he needs, as far as the continuing benefit is concerned, when the interest rates change from that illustrated.

- 1871-1, NAIC Proc.

-

- 1983 - SOA - Universal Life, Society of Actuaries - 24p

- Broken down to its simplest basis, Universal Life has eliminated the concept of "plan of insurance" ... -- Christian J. DesRochers

- 1979 - SOA - Future Trends and Current Developments in Individual Life Products, Society of Actuaries - 24p

- If that is the case, how does an agent program somebody?

- How does he tell a person what he needs to pay to keep his premiums level or to have paid-up insurance at age 65? -- Allan W. Sibitroth

- 1983 - SOA - Universal Life, Society of Actuaries - 24p

-

- 1984-2, NAIC Proc. - Report Of The (EX3) Market Conduct Surveillance Task Force Working Group On Consumer Complaint Analysis

- As a member of a regulatory body it is important that you become involved in self-education to increase your professional knowledge and keep current on developments within the ever-changing business of insurance.

- 1985 0719 Impact of Tax Reform on Insurance Industry, Pete Stark (D-CA) --- [BonkNote]

- Robert Beck, Prudential, Chairman and Chief Executive Officer

- RE: Vanishing Premium

- Under some permanent insurance, contracts being sold today, the chances are you could stop paying after 7, 8, or 9 years and the insurance would remain in force for the rest of your life without further premium payments. (p6069)

- [VIDEO-CSPAN] - Impact of Tax Reform on Insurance Industry - (at approx. 2:27:00-2:27:30)

- Robert Beck, Prudential, Chairman and Chief Executive Officer

- 1986 - SOA - Variable Life/Fixed and Flexible Premium, Society of Actuaries - 38p

- We were very unenthusiastic latecomers to universal life.

- Gilbert W. Fitzhugh, Senior Vice President and Actuary at PRUCO Life, stock subsidiary of the Prudential Insurance Company

- We were very unenthusiastic latecomers to universal life.

- 1989-1, NAIC Proceedings - Society of Actuaries - Task Force on Nonforfeiture Principles Interim Report-Tentative Conclusions (p612-?)

- Unlike adjustable life, where a current plan is defined, but is subject to change, a universal life policy at any time has only a "minimum" and a "maximum' plan.... (p662)

- 1990-1A, NAIC Proceedings - NAIC / LIMRA - Universal Life Disclosure Form Focus Group Summary, Consumer Issues Disclosure Working Group --- [BonkNote] --- 10p

- A great deal of the confusion seems to stem from a lack of understanding of how cash value insurance products work....

- Also, because most people presume that if you pay your premium continuously, your policy will remain in effect, quite a few people had a hard time understanding how or why the policy would terminate in policy year 31.

- This was simply foreign to their way of thinking.

- One person was so confused that he said that the maturity age and endowment benefit were moot points, since the policy was going to end at year 31 anyway."

- 1984-2, NAIC Proc. - Report Of The (EX3) Market Conduct Surveillance Task Force Working Group On Consumer Complaint Analysis

-

- 1993-1, NAIC Proceedings - (EX Special Committee op Metropolitan Life, December 17 1993 - Conference Call - p43

- 1. Discussed the charge of the committee and described the problem as one where agents have been found to be marketing a life insurance product as an annuity/retirement product, particularly targeting consumers from business and professional associations, such as nurses and cosmetologists.

- 1993 0307 - NYT - States Set Fines for Met Life, by Michael Quint - [link]

- The Florida Report - <WishList>

- The improper activities involved sales of life insurance policies to customers who were told by sales agents that they were buying a retirement or savings plan, the report said.

- The Florida Report - <WishList>

- 1993 0525 - GOV (Senate) - When Will Policyholders Be Given The Truth About Life Insurance?, Howard Metzenbaum (D-OH) --- [BonkNote]

- (p4) - Statement of Hon. Charles E. Grassley, A U.S. Senator From The State of Iowa

- I share Senator Metzenbaum's desire to ensure that insurance consumers have a thorough understanding of the obligations and performances that they can expect from a prospective life insurance policy, so that they can make fully informed purchase and investment decisions.

- (p4) - Statement of Hon. Charles E. Grassley, A U.S. Senator From The State of Iowa

- 1993-4, NAIC Proceedings - Tony Higgins (NC) agreed that there was a problem with lack of education of the agents.

- 1993-4, NAIC Proceedings - Life Disclosure Working Group – NAIC

- The working group's concern was how to bring about a change without damage to the market place.

- 1993 - SOA - Sales Illustrations - We Can't Life With Them, But We Can't Live Without Them!, Society of Actuaries - 28p

- -- Bruce E. Booker, (a member of the American Council of Life Insurance (ACLI) Task Force on Cost Disclosure and the National Association of Insurance Commissioners (NAIC) Advisory Group on Illustrations

- Actuaries can do lots of things.

- We can provide the field with a clear description of the policy and how it works.

- Robert Nelson, Chairperson of the National Association of Life Underwriters (NALU) Task Force on Illustrations - [Currently NAIFA]

- I sincerely believe we have a flawed instrument in today's sales illustrations.

- ...we did not communicate the impact of change as well as ...we should have.

- Our biggest mistake would be to delay.

- I don't believe the consumer will tolerate or forgive us, let alone the regulators, if we do nothing.

- -- Bruce E. Booker, (a member of the American Council of Life Insurance (ACLI) Task Force on Cost Disclosure and the National Association of Insurance Commissioners (NAIC) Advisory Group on Illustrations

- 1994-1, NAIC Proc.

- As the cases of Metropolitan Life and Prudential suggest, no amount of oversight or self-policing will protect consumers from unethical or illegal company and agent practices.

- The structure of the market needs to change."

- Consumers Union

-

1994 0613 - APNews - Life Insurance Buyers Allege Misleading Sales Tactics Were Used With PM-Vanishing, by Mark Dennis - [link]

- 1995-1, NAIC Proceedings

- Fred Nepple (Wis.) asked: if a charge was not rational, did that mean it could not be charged or it could not be illustrated?

- The working group agreed that the result was that it could not be illustrated.

- 1995 - SOA - Practical Illustrations and Nonforfeiture Values, Society of Actuaries - 14p

- Mark J. Greene, FSA. MAAA, Supervising Actuary, New York State Insurance Department

- What I noticed was there is a requirement for in-force illustrations, and people may have thought they bought one thing and whenever you have to give them an in-force illustration with a current disciplined scale, they're going to realize they bought something else.

- I think many companies will have serious problems with policyholder retention.

- Mark J. Greene, FSA. MAAA, Supervising Actuary, New York State Insurance Department

- 1996 05 - Report of The Multi-state Life Insurance Task Force and Multi-state Market Conduct Examination of The Prudential Insurance Company of America - By the Examiners of The Multi-state Life Insurance Task Force From Several State Departments of Insurance and other State Regulatory Agencies - 270p

- 33 percent of the sales complaints concerned misrepresentation by agents in the course of a sale. (p8)

- Such complaints were not new, but due to recent media attention and other factors, have been received and handled in large numbers. (p12)

- There is ample evidence to suggest that many of the practices at Prudential are, or were, present at other life insurers.

- 1993-1, NAIC Proceedings - (EX Special Committee op Metropolitan Life, December 17 1993 - Conference Call - p43

-

- 1996 - SOA - Nonforfeiture Law Developments, Society of Actuaries - 23p

- Larry Gorski, Illinois Insurance Department - Actuary

- They are complaints about things that we can’t do anything about because the contract might be a universal life type product with nonguaranteed elements, and there is no regulatory framework to deal with those issues.

- Those complaints just fall by the wayside because there is nothing that can be done.

- Larry Gorski, Illinois Insurance Department - Actuary

- MDL-1061 – Prudential Insurance Company of America Sales Practices Litigation

- 1999 - SOA - The Next Generation Universal Life, Society of Actuaries - 30p

- The actual versus expected performance for some Universal Life policies led to class-action lawsuits that have caused a substantial amount of negative attention to be focused on cash-value life insurance in the illustration of projected values. --- Deanne Osgood, Milliman & Robertson

- 2000-1, NAIC Proceedings - March 14, 2000

- (p81) - Thomas Foley said the working group had been charged to make amendments to the Life Insurance Disclosure Model Regulation - (Attachment Three-A) to be consistent with the Life Insurance Illustrations Model Regulation adopted in 1995.

- (p83) - Thomas Foley said that for a variable product, if the 12% illustration is used, it can show a very low premium for coverage.

- If the policy does not attain the 12% return it will not be a permanent policy.

- He opined that consumers are misled if the 12% is not a reasonable amount over time and consumers are in the same position as they were in the 1980s when "vanishing premiums" were touted.

- 2001-1, Suitability Working Group - NAIC

- Ron Panneton (National Association of Insurance and Financial Advisors -- NAIFA) said most of the comments from his association focused on whether the regulation should apply to recommendations and sales or just to recommendations that result in sales.

- He said the company has an obligation to draft guidelines for producers and to make sure they are used.

- The company should have the ultimate responsibility for unsuitable sales because it should look at the applications that come in.

- He urged the working group to consider both sales and recommendations.

- Ron Panneton (National Association of Insurance and Financial Advisors -- NAIFA) said most of the comments from his association focused on whether the regulation should apply to recommendations and sales or just to recommendations that result in sales.

- 2002-2v1, NAIC Proceedings - Mike Velotta (Allstate Life) ... said that the industry is regulated more by class action litigation than state law.

- 2002-2v2, NAIC Proceedings - 2002 0608 - Industry Representatives White Paper on Class Action Lawsuits Preserving The Regulatory Authority of State Insurance Commissioners, Preliminary Draft - p1609-1612

- 2002 0731 - GOV (Senate - Committee on the Judiciary) - Class Action LItigation - [PDF-178p]

- (p55) - ACLI - Patrick Baird

- The life insurance industry has experienced over a decade of abusive class actions.

- In one of the more recent examples of such class action abuses.

- State courts in New Mexico are certifying nationwide classes of plaintiffs for the manner in which their premiums are disclosed in their policies.

- These cases are being certified even though State Commissioners of Insurance reviewed and approved these policy disclosures.

- These class action cases have steadily weakened the very fabric of State regulation of insurance as the State judges' decisions have had national implications for insurers in other states.

- The result of nationwide regulation through targeted class action litigation has indirectly usurped the role and authority of the State Commissioners of Insurance.

- (p55) - ACLI - Patrick Baird

- 2003 - SOA - Do You Know How Much You're Spending? The Hidden Costs of Product Complexity, Society of Actuaries - 19p

- UL is a horror. Who understands UL?

- The home office doesn't.

- The IT department doesn't.

- The owner doesn't.

- Jeff Robinson

- UL is a horror. Who understands UL?

- 2003-2, NAIC Proceedings - ATTACHMENT THREE-A - Outline of White Paper on Class Action Lawsuits

- 2003 - LC - Fay v Aetna - Doc 65 - Defendant Aetna Life Insurance And Annuity Company's Response To Plaintiffs' Separate Statement of Additional Undisputed Material Facts - 01-cv-10846 - 32p

- 20. Aetna does not dispute that Mr. Pflugfelder described the Policies as "permanent insurance."

- He did so correctly, as Plaintiffs concede.

- 21. Aetna does not dispute this paragraph, but adds that Plaintiffs never asked what the term "permanent insurance" means. - Page 6 of 32

- 20. Aetna does not dispute that Mr. Pflugfelder described the Policies as "permanent insurance."

- 2007 - IAA (International Actuarial Association) - Measurement of Liabilities for Insurance Contracts: Current Estimates and Risk Margins, IAA ad hoc Risk Margin Working Group - 170p

- (p156) - E6.2.3 - The following are some considerations that can affect expected discontinuance assumptions.

- The way the contracts were sold and marketed (e.g., a universal life contract sold as low premium term insurance or primarily for investment purposes).

- (p156) - E6.2.3 - The following are some considerations that can affect expected discontinuance assumptions.

- 2007 1030 - GOV (House) - Additional Perspectives on the Need for Insurance Regulatory Reform, Paul Kanjorski, (D-PA) - [PDF-180p, VIDEO-Archive.org]

- (p10-11) - Statement of J. Robert Hunter, Director of Insurance, Consumer Federation of America

- There are problems waiting to emerge that will be uncovered by lawsuits, not the regulators, or by the media.

- Consider life insurance market conduct abuses of a decade ago.

- The largest life insurers told people their premiums would disappear, and confused them into believing their life insurance was an investment.

- It took lawsuits to uncover these problems.

- [Bonk: Vanishing Premium, LIRP - Life Insurance as a Retirement Plan]

- (p10-11) - Statement of J. Robert Hunter, Director of Insurance, Consumer Federation of America

- 2016-2, NAIC Proceedings - 2016 0516 - LIIIWG - Life Insurance Illustrations Working Group, Conference Call

- Teresa Winer (GA) asked if it would be useful to ask states whether they have received consumer complaints about the summaries.

- Richard Wicka (Chair - WI) said that it would be helpful to have that kind of information but that he is not sure it would be possible to track down complaints to that level of detail. (6-161)

- 2019 0903 - NAIC - LIIIWG - Life Insurance Illustrations Working Group, Conference Call - [Bonk: Not in NAIC Proceedings]

- Teresa Winer (GA): I'm guessing that, perhaps, this came out of the fact that Illustrations were not as clear.

- Maybe there's been complaints.

- And the purpose of this entire committee was to provide some kind of summary to make it a little bit more clear.

- Teresa Winer (GA): I'm guessing that, perhaps, this came out of the fact that Illustrations were not as clear.

- 1996 - SOA - Nonforfeiture Law Developments, Society of Actuaries - 23p

Legal Cases

- bonknote.com/legal-cases-index/

- 1990s -

- 2000-2009

- 2009 - Legal Case - Blumenthal v New York Life --- [BonkNote]

- 2010-2020

- 2010 - Legal Case - Maloof v. John Hancock Life Ins. Co. - 60 So. 3d 263 - Alabama Supreme Court Opinion --- 39p --- [BonkNote]

- Walker v Life Insurance Company of the Southwest

- 2014 0425 - DOC 813 - Trial Transcript - Walker v LSW - 224p - [BonkNote]

- Closing Argument by Mr. Martens, Defendant Attorney, Life Insurance Company of the Southwest - LSW

- (p171) - (p170) - Mr. Brosnahan said: Well, the fees can cause policies to lapse. Is that a secret?

- I mean, fees cost something. That's the point of fees. If someone puts money into their policy, there will be fees, as they know, coming out of those policies.

- If you don't put enough premiums into your policy, over time the fees will keep decreasing the value of the policy. That's what fees do.

- That's not a defect in the policy. That's how policies work.

- (p171) - The fact that we charge people fees that we have disclosed and that fees reduce the value of your policy, and if your policy keeps reducing in value, it will lapse, is not a fraud.

- That's common sense.

- That's how life insurance works.

- 2014 0425 - DOC 813 - Trial Transcript - Walker v LSW - 224p - [BonkNote]

- Walker v Life Insurance Company of the Southwest (LSW) - DOC 810 - Trial Transcript - Day 7 - Joyce Walker - 260p

- (p27-30) - Q And did you end up sending the letter to the California Department of Insurance?

A Yes.

Q And did you at any point after the complaint was filed with the Department of Insurance have contact with anyone at the department with respect to your complaint?

A Yes. Christine Wilton.

Q And did you exchange e-mails with Ms. Wilton during the process of her investigation? - (p28) - A Yes.

Q Would you take a look at Exhibit 733. Is that one of the e-mail exchanges you had with Ms. Wilton at the Department of Insurance?

A Yes, it is.

Q And had you had a number of communications with Ms. Wilton prior to the January 21, 2010, e-mail, Exhibit 733?

A Yes.

Q And to your knowledge had Mr. Burgess also spoken with her a number of times?

A Yes.

Q And Ms. Wilton, was she a lawyer with the Department of Insurance?

A Yes, sir.

Q Reading from your e-mail, 733: Thanks again for staying with me on this LSW policy. Sounds like you might have found an omission that just might work in my favor in terms of getting all my money back. The lack of stated reason for an amount percentage of fees taken out every month could be the loophole I need. What did you understand about the omission she may have found with respect to the fees?

A I understood that it had to do with something with the fee structure. - (p29) - Q And what did you mean when you said the omission about fees could be the loophole that you needed?

A Well, like you said, Christine is a lawyer. Her area of expertise is insurance law. She indicated that there was an omission --

MR. SHAPIRO: Objection, Your Honor. Nonresponsive.

THE COURT: Sustained. This part of the answer will be stricken.

BY MR. FREIBERG:

Q What did you understand from what she said?

A I understood that there was a possibility and that I was encouraged that she had found something that I might be able to use against the defense that LSW was saying I signed my contract and I had no other recourse.

Q Did the Department of Insurance ultimately take any action with respect to your complaint?

A No, they did not.

Q Did you receive a letter to that effect?

A Yes, I did.

Q And is Exhibit 668 that letter?

A Yes, it is.

Q And that letter is from Christine Wilton, the lawyer with whom you had been communicating at the Department of Insurance? - (p30) - A Correct.

Q In this letter does Ms. Wilton tell you the following: As a regulatory agency, the Department of Insurance does not have the authority to resolve complaints where the allegations are based upon undocumented conversations. This department may not be your final resource. You may wish to seek the advice of an attorney or pursue the matter in Small Claims Court. I regret the department was unable to assist you. Thank you for contacting us with your concerns. Is that what you received?

A Yes.

Q Did you speak with Ms. Wilton after you received this letter?

A I did.

Q What did she say?

MR. SHAPIRO: Objection, Your Honor. Calls for hearsay.

MR. FREIBERG: Same, Your Honor.

THE COURT: Not for the truth.

THE WITNESS: We had some discussion and ultimately she recommended that I have a forensic analysis done on this policy.

BY MR. FREIBERG:

Q What did you understand a forensic analysis meant?

A That there might be something more to it that she had yet to discover as well.

- (p27-30) - Q And did you end up sending the letter to the California Department of Insurance?

- I think you have to catch people's attention, and that is all to the good.

-- George Coleman, Prudential, TRG-Technical Resource Group for the NAIC (Industry Advisory Group - Illustrations)

1994 - SOA - Problems and Solutions for Product Illustrations, Society of Actuaries - 28p

- There is bound to be a controversial element in anything that enlightens the public to these differences and gives them a more intelligent basis for choice than they have at the present time.

1977 - SOA - Debate Resolved: The Life Insurance Business as Transacted Today is in its Terminal States, Society of Actuaries - 14p

- 2023 0410 - MAPWG / NAIC - Virtual Meeting - 9p

- p1 - 2. Discussed its Charges and Goals for 2023

- LeDuc said all last year’s charges remain, but one additional charge was added by the Market Regulation and Consumer Affairs (D) Committee.

- She said the new charge is to, “assess currently available market analysis data to identify needed improvements in the effectiveness of the data for market analysis and the predictive abilities of the market scoring systems utilizing the data.”

- She said this charge is also included in the Market Information Systems (D) Task Force charges, and the Working Group will report to the Task Force its progress throughout the year. [MIS/AI]

- LeDuc reminded the Working Group that the Task Force charged the Market Information Systems Research and Development (D) Working Group to research and make recommendations surrounding the incorporation of artificial intelligence (AI) techniques into the NAIC’s Market Information Systems (MIS). She said the Working Group’s recommendations were discussed by the Task Force and ultimately adopted by the Task Force at the 2022 Summer National Meeting. She said while the report was generally favorable to incorporating AI techniques into the MIS, it recognized that the data used in the MIS is not as complete as would be needed for AI to be useful. Additionally, the effectiveness of the data collected and the scoring systems likely need improvement.

- LeDuc said she and Haworth are suggesting that the best place to start is to hear from the Working Group members and other interested state insurance regulators about what data they use, how they use the data, and their thoughts on the data’s effectiveness. She said the only scoring systems currently in the MIS are the Market Analysis Prioritization Tool (MAPT) scoring and the Market Conduct Annual Statement (MCAS)-MAPT rankings. She said the Working Group will consider these later in the year, but the Working Group should first dedicate itself to the effectiveness of the data, because if the effectiveness of the data is not good, the scoring will also be lacking.

- LeDuc said all last year’s charges remain, but one additional charge was added by the Market Regulation and Consumer Affairs (D) Committee.

- ⇒ p2 - LeDuc asked for comments to be sent to Randy Helder (NAIC) by April 28 regarding the data used by jurisdictions and the effectiveness of the data

- p5-7 - Potential Data Sources Used in Market Analysis

- p1 - 2. Discussed its Charges and Goals for 2023

- 2021 1014 - NAIC - Review of Artificial Intelligence Techniques in Market Analysis - The Market Information Systems Research and Development (D) Working Group - 15p

- Executive Summary

- This report fulfills the Market Information Systems Research and Development (D) Working Group charge to evaluate the potential benefits of artificial intelligence (AI) in relation to market analysis.

- Current Status of Market Analysis

- Quantitative market analysis relies on just a handful of data sources:

- Miscellaneous Data Sources:

- Insurers that are under financial stress, or that rapidly expand into or contract out of a line of business, or that exhibit high defense or other adjudication costs, may be subjected to additional analysis.

- Miscellaneous Data Sources:

- p4 - An important caveat is that predictive analytics is not well developed in market regulation.

- Potentially, AI methods could assume many of the functions that are currently performed manually.

- For example, many of the pattern-seeking analysis performed by analysts in a level 1 review could conceivably be more efficient if automated.

- Potentially, AI could identify patterns that might elude a human analysis.

- A very advanced level of AI could perhaps assume complex analysis involved with manually reviewing complaint files and documents.

- However, while the possibility is raised here, it is not further pursued.

- That level of AI suitable for tasks may not even exist as yet, or if it does, it may be so specialized that it may not be available to state insurance regulators.

- Even if available, the likely enormous costs themselves would render them highly impractical.

- Quantitative market analysis relies on just a handful of data sources:

- I. Existing Market Analysis Data

- As noted above, market analysis suffers from a paucity of detailed data.

- (p5-7) - Potential Data Sources Used in Market Analysis

- Executive Summary